Is the UK Actually Getting Poorer?

GDP in the UK has steadily risen over the last decade - and yet, people feel poorer, with pressure from stagnant incomes, rising inequality, and unaffordable housing constraining living standards.

For many individuals in the United Kingdom, the perceived return on effort- through wages, career progression and asset ownership- has weakened significantly. While academic and labour market competition has always existed, this alone does not explain the growing sense of economic frustration. Economic decline is often difficult to define. On paper, the United Kingdom remains one of the world’s largest economies, ranking 6th and 20th in GDP per capita (with GDP broadly recovering after the COVID-19 pandemic).

On aggregate measures, the UK appears economically strong , so why is it that people feel poorer? This essay argues that while the UK is not “poorer” in aggregate GDP terms, it is becoming poorer in real per capita and distributional terms. Stagnant incomes, rising inequality, unaffordable housing and weakening labour market outcomes all point towards a sustained decline in living standards.This raises an important question: Is the UK actually getting poorer? The paradox between what headline indicators suggest and what households actually experience is not merely perceptual, it reflects genuine structural deterioration in the foundations of economic wellbeing.

Stagnant real incomes and living standards

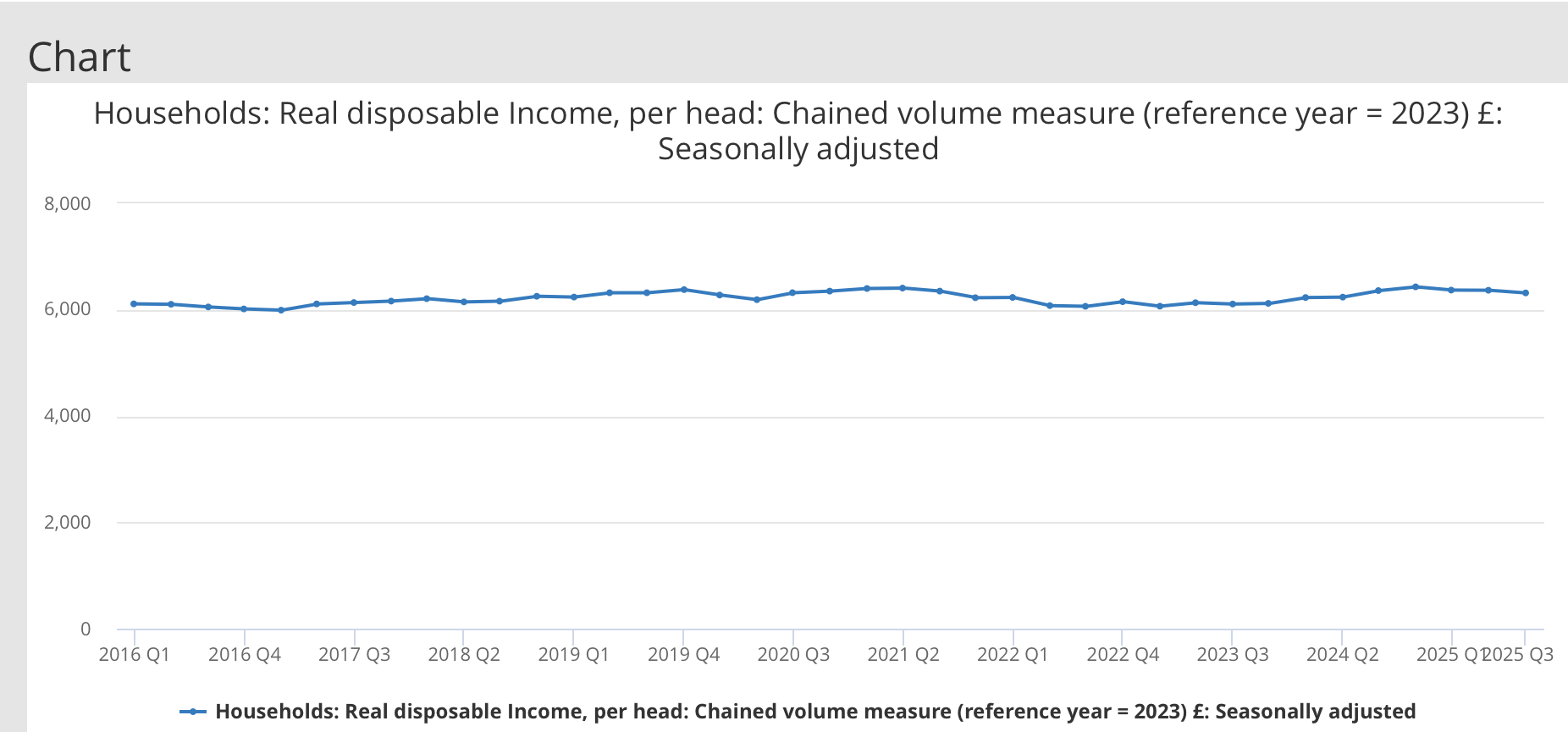

The clearest indicator of whether a country is “getting poorer” is real disposable income (RDI) which is adjusted for inflation. Unlike nominal income, which can rise simply due to price increases, real income reflects actual purchasing power and therefore living standards. Since the 2008 financial crisis, UK real incomes have experienced an unprecedented and extended period of stagnation. Over the last decade, real disposable income per head has remained around £6,100, representing a cumulative increase of less than 5%, - a period economists usually describe as a lost decade (ONS 2025)

According to recent estimates,the average UK household would be earning £10,200 more if pre-2010 trends had continued.This reflects not an absolute decline in income, but a significant shortfall relative to expected economic progress. Unlike a typical recession, where incomes fall sharply before recovering, this is gradual erosion of living standards; households feel poorer over time as they have the same disposable income for many years. Incomes have not collapsed, but their failure to grow meaningfully alongside rising prices has steadily reduced purchasing power over time. This makes stagflation particularly dangerous, particularly for prolonged periods of time. This matters because when real income fails to grow, household consumption weakens, business confidence falls and opportunities for upward mobility diminish. As Duesenberry (1949) argues, individual economic satisfaction is determined not only by absolute income, but by one’s position relative to others in the same social group.

Inflation vs Wage Growth: The cost of living crisis

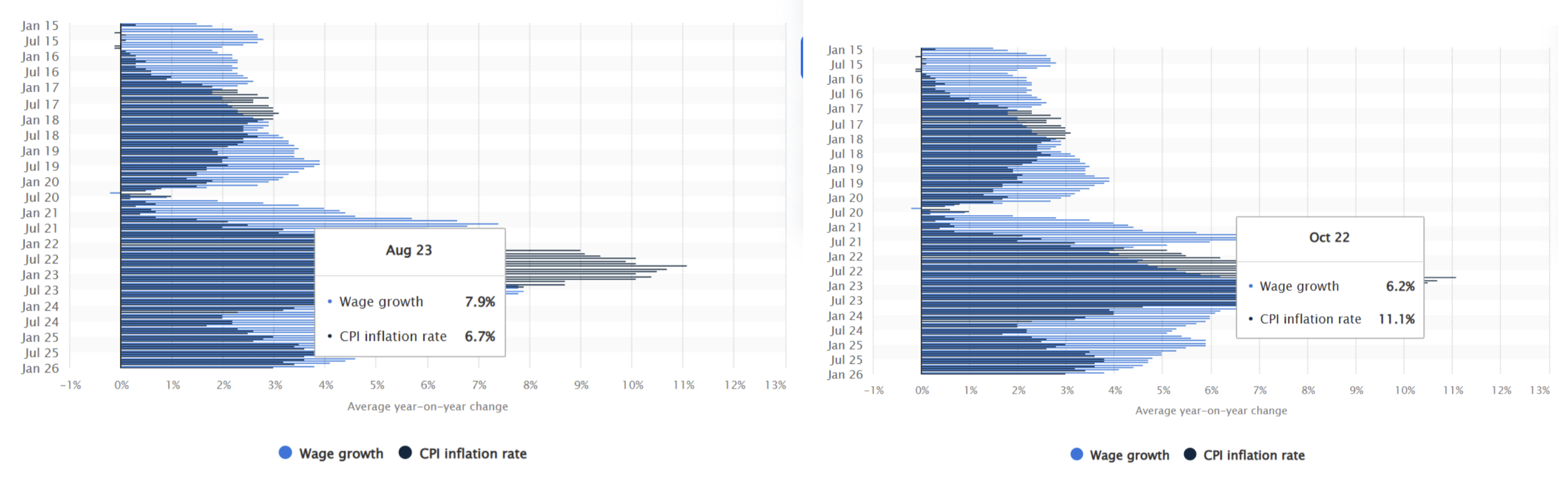

Has inflation fallen below wage growth? Inflation is the rate at which the price level of goods/services tends to rise.As people, as our income rises, so does our disposable income.This allows us to buy discretionary goods and services.This means that for living standards to remain stable, wage growth must at minimum keep pace with inflation. However, this wasn’t the case between January 2022 and October 2024. Between this period of time , CPI inflation peaked at 11.1% while wage growth only reached 7.9%.

This 3.2% shortfall constituted a real-terms pay cut for the vast majority of workers (ONS CPIH series). Therefore, individuals can now purchase fewer goods/services than they could have in the previous years even though their nominal salary increased. Consider a worker earning £35,000 in early 2022. The inflation rates reached a record high of 11.1% and Consumer Prices Index including owner occupiers’ housing cost (CPIH) over the period of Jan 2022- Oct 2024 at 17%. This means a worker earning £35,000 in early 2022 would now need around £40,950 to maintain the same purchasing power.

The effects of economic changes as drastic as those are not limited to the period of time they occurred. Inflation measures the rate of price change, not the price level itself. Even as inflation fell to 3% by January 2026- a nominal wage growth of 3.8% now marginally ahead- goods and services remain significantly more expensive in absolute terms than before 2022. If a good cost £10.00 in Jan 2022, it would cost approximately £11.43 today. Those elevated prices do not disappear when inflation falls, they become the new baseline from which further increases compound.

As a result, the Purchasing Power of many households is likely to stay constrained for a few more years, regardless of recent headlines showing improvement. The cost of living crisis isn’t a closed book, effects are still felt today.

Prices and housing Affordability

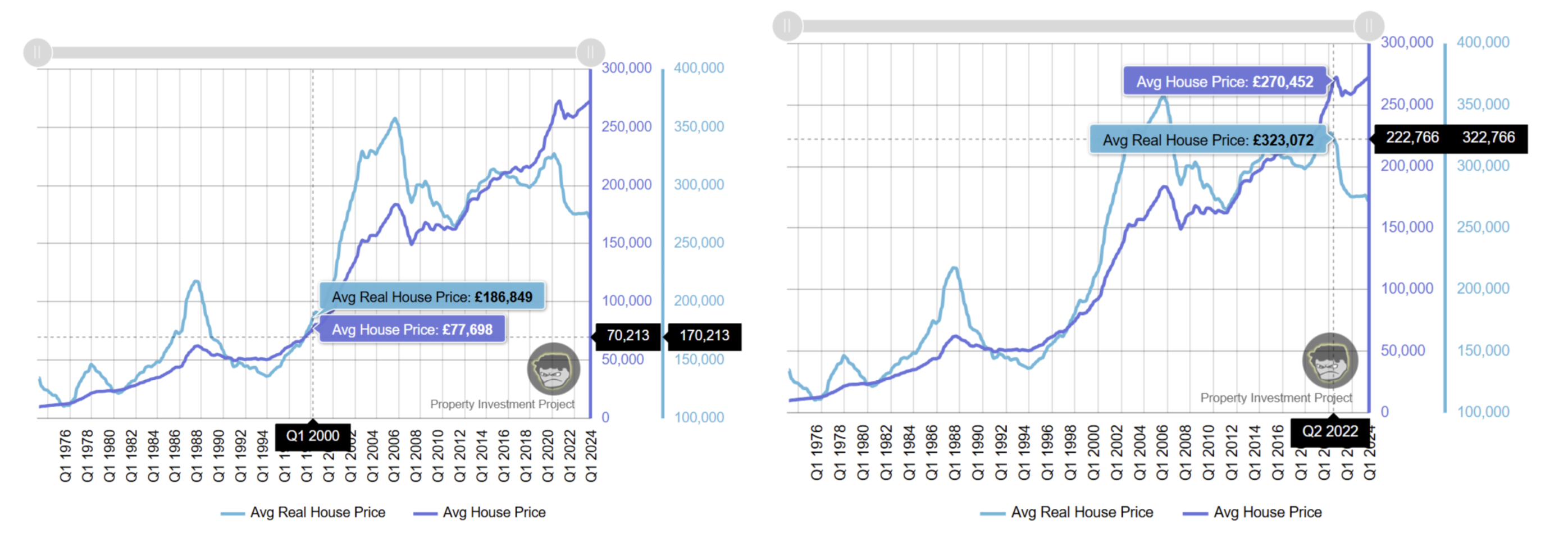

In the UK, wealth is often held, not in liquid assets, but in property. Homeownership represents a primary vehicle through which ordinary households accumulate long term financial security.However,access to that vehicle has become increasingly out of reach.The house price to median income ratio just reached 8.3 in 2025 (this means the average house price is 8.3 times the gross annual salary of a typical worker.) and this ratio is projected to remain above 8.0 throughout 2026

When adjusted for inflation, the average UK house price rose from approximately £186,800 in 2000 to over £272,000 in 2025 - an increase of around 46% in real terms.(ONS Wealth and Assets Survey) This suggests that rising house prices are not merely a reflection of general inflation, but a structural increase in housing costs relative to incomes, meaning homes have become genuinely more expensive in real terms, not simply nominally more expensive due to a depreciating currency.

Consider a dual-income household where both individuals earn the average salary for 30-39 year olds(£45,105), giving each household a combined gross income of £90,210. Saving 12% of net income, such a household would require 3-4 years to accumulate a 10% deposit and 6-7 years for a 20% deposit- and these are optimistic assumptions. In practice, high rental costs, increasing energy bills and just normal living expenses would severely decrease the capacity to save, pushing realistic timelines further. The impact is that many households in sustained full-time employment cannot enter the housing marker until their late 30s, a delay that substantially makes wealth accumulation take longer and reinforces the sense that younger generations are worse off than those before them.

Inequality and MPC

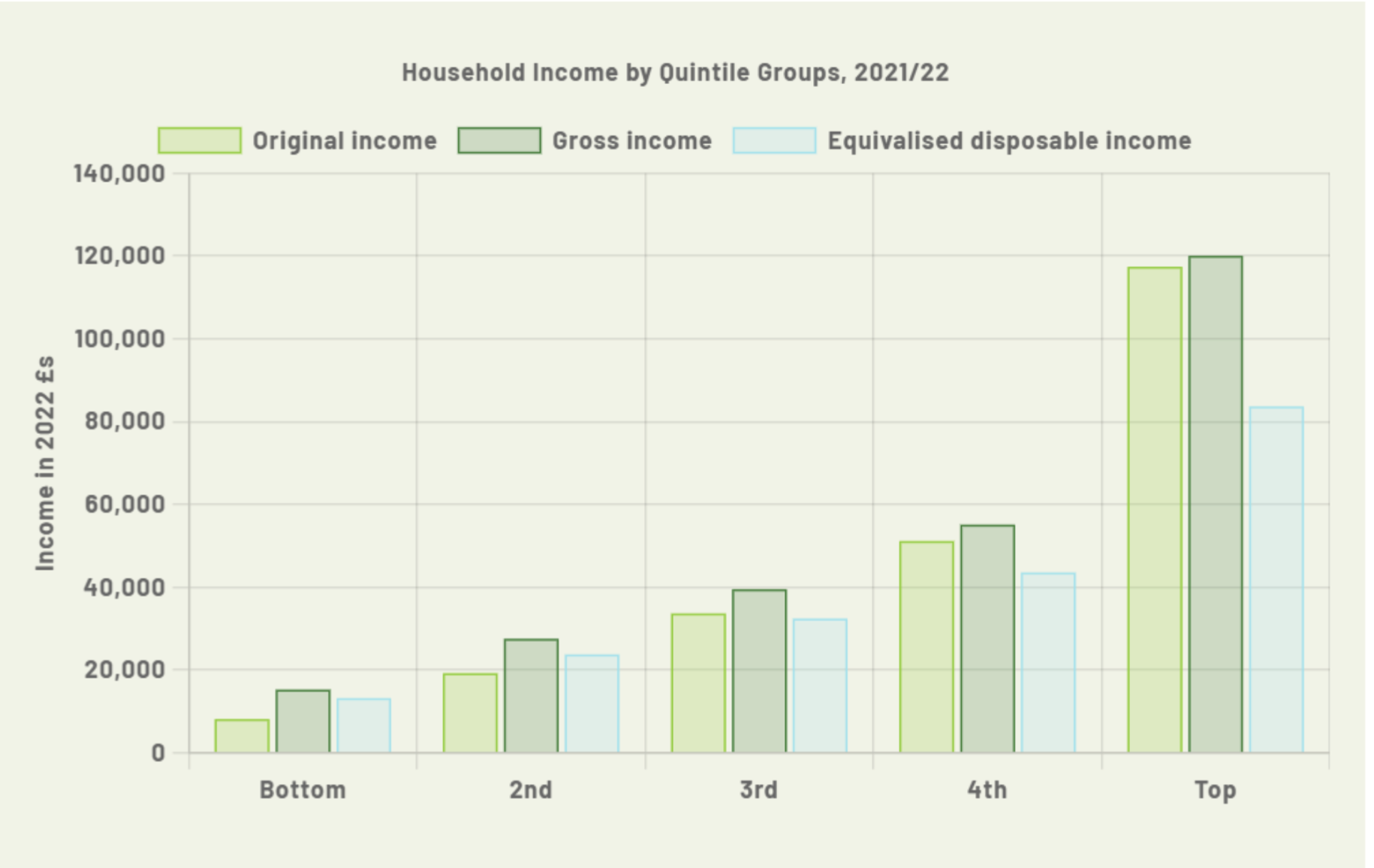

Income inequality compounds all of the above pressures. In 2021/22, the lowest 20% of UK households had an average disposable income of £13,218, compared to the £83,687 for the highest 20%- a ratio exceeding 6:1 (Equality Trust,2022). On pre tax, pre transfer incomes, the top quintile earned more than 12x the bottom quintile. Research published by the London School of Economics found that the UK’s wealth gap (measured in accumulated assets) grew by 50% over the last eight years to 2024(Snell, 2024).

One of the UK's macroeconomic objectives, however ever so evidently on the bottom of their list. Is wealth distribution making the economy feel poorer? A millionaire living amongst lower middle class people whose incomes are set around £45,000. The marginal propensity to consume of the millionaire and the lower middle class people will be completely different. The Bank of England found that households concerned about not being able to make ends meet have a 20% higher MPC than other households meaning lower-income households spend a significantly larger share of each additional pound than higher-income households, who tend to save more. As income becomes increasingly concentrated among those with low MPC’s, aggregate demand weakens. Consumer spending grows more slowly and the multiplier effect diminishes so the economy loses the self reinforcing cycle of income, spending and growth that underpins rising living standards.

Addressing this dynamic involves a policy trade-off. While redistributing income or discouraging excessive saving could stimulate consumption, overly restrictive policies may reduce incentives for investments. High-income individuals and firms may respond by reallocating capital abroad, limiting domestic investment and potentially weakening long term economic growth.

Labour Market and Job Quality

The difficulty of securing stable,well-paid employment(particularly in professional roles) is well documented and increasingly prevalent. Survey data shows77% of workers prioritise job security over salary. The aim isn’t “how much am I getting paid?” anymore, it has significantly shifted to “Will I be able to keep a job for a couple years?” In addition, 71% of people are actually now hesitant to change careers due to the lack of stability in other firms(People Management,2014). This shift reflects a fundamental change in labour market confidence. When workers prioritise security over advancement, consumer spending weakens which isn’t good for the economy.

Approximately 20% of job seekers in the UK have been searching for jobs for the past 10-12 months(Calibre, 2024). This prolonged absence from the labour market represents a loss of potential output, productivity and progressive erosion of human capital. If these 20% had found employment, what could the implications have been for the economy? Productivity, tax revenue and aggregate demand would increase. The opportunity cost of prolonged unemployment is a drag on economic performance.

The Case against Decline

A balanced analysis requires engaging seriously with the evidence on the other side.The UK retains economic strength on paper. GDP has largely recovered to pre-pandemic levels, suggesting that overall economic output remains resilient. Inflation peaked at 11.1% in October 2022 but has since fallen to 3% which is still within the Government's target(so technically this is a very good sign) which eases pressures on households finances and restoring modest real wage growth for the first time in years. Furthermore, levels of employment remain relatively high by historical standards, indicating a degree of labour market stability.

Alternatively, these improvements must be interpreted with caution. Falling inflation does not imply falling prices, but rather a slower rate of increase.Similarly, recent real wage growth follows a prolonged period of stagnation during which purchasing power substantially declined. As a result, although the economy may be stabilising in the short run, these improvements do not necessarily translate into a meaningful recovery.

Overall Outlook

Whether the UK is “getting poorer” is dependent on measures of economic performance. In aggregate output terms, the UK remains a major economy with resilient headline indicators and genuine sectoral strengths so the claim of outright decline appears overstated.

But this view obscures a more troubling reality at the level of households and individuals. Real income growth has been negligible for over a decade. Housing has become structurally unaffordable for working households across much of the country. Income and wealth inequality have widened, suppressing aggregate demand. Labour market quality has deteriorated even where employment rates appear stable. The cumulative effect is an economy that grows on paper, yet consistently fails to translate that growth into broad improvements in living standards.

The most accurate characterisation is not collapse, but stagnation- and in some respects, quiet regression. Until the gap between aggregate economic performance and lived experience of ordinary households begin to narrow, the perception that the UK is getting poorer will remain not merely understandable, but economically well founded

How to cite

Timi Idowu (2026). "Is the UK Actually Getting Poorer?". Future Economists Institute.